For aircraft owners, buyers & leaseback operators

The financial intelligence platform for aircraft ownership.

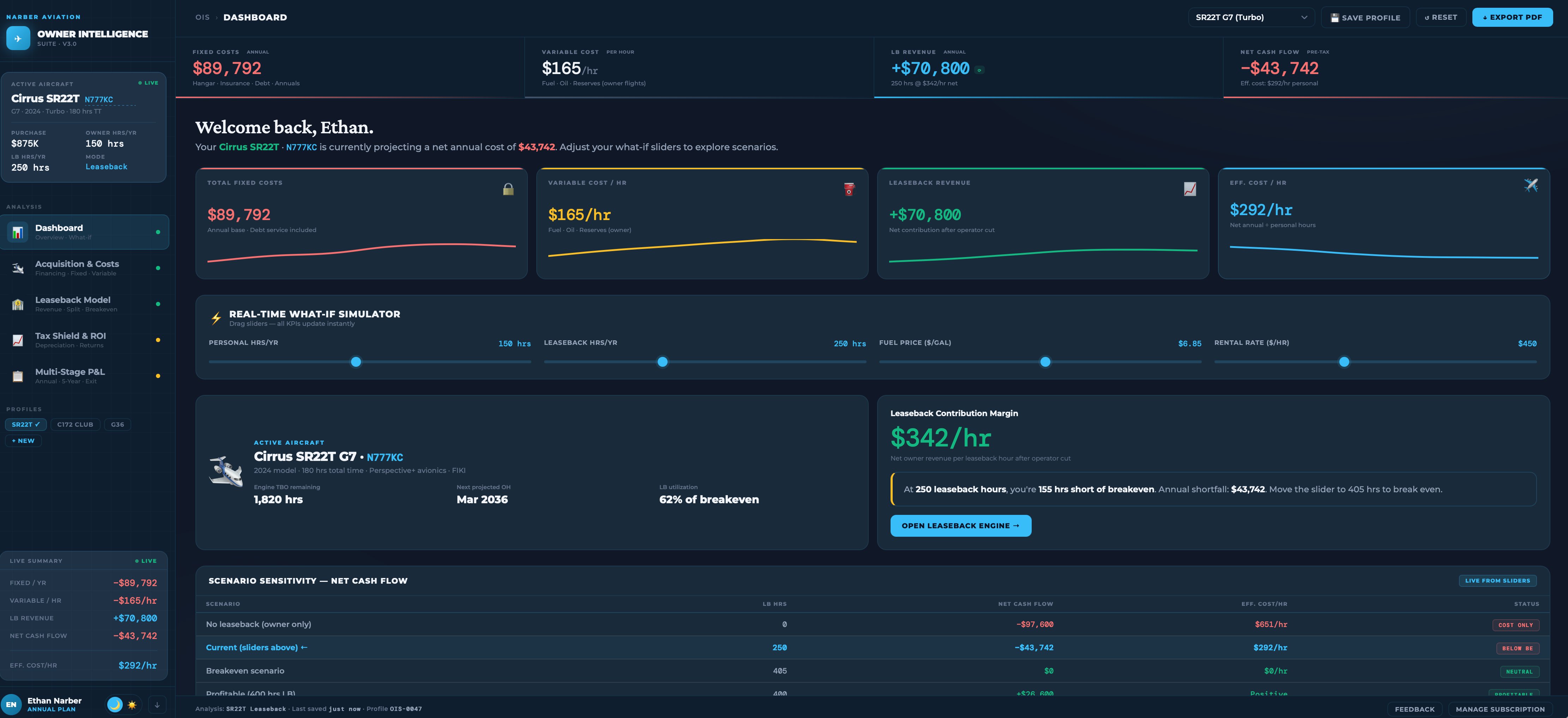

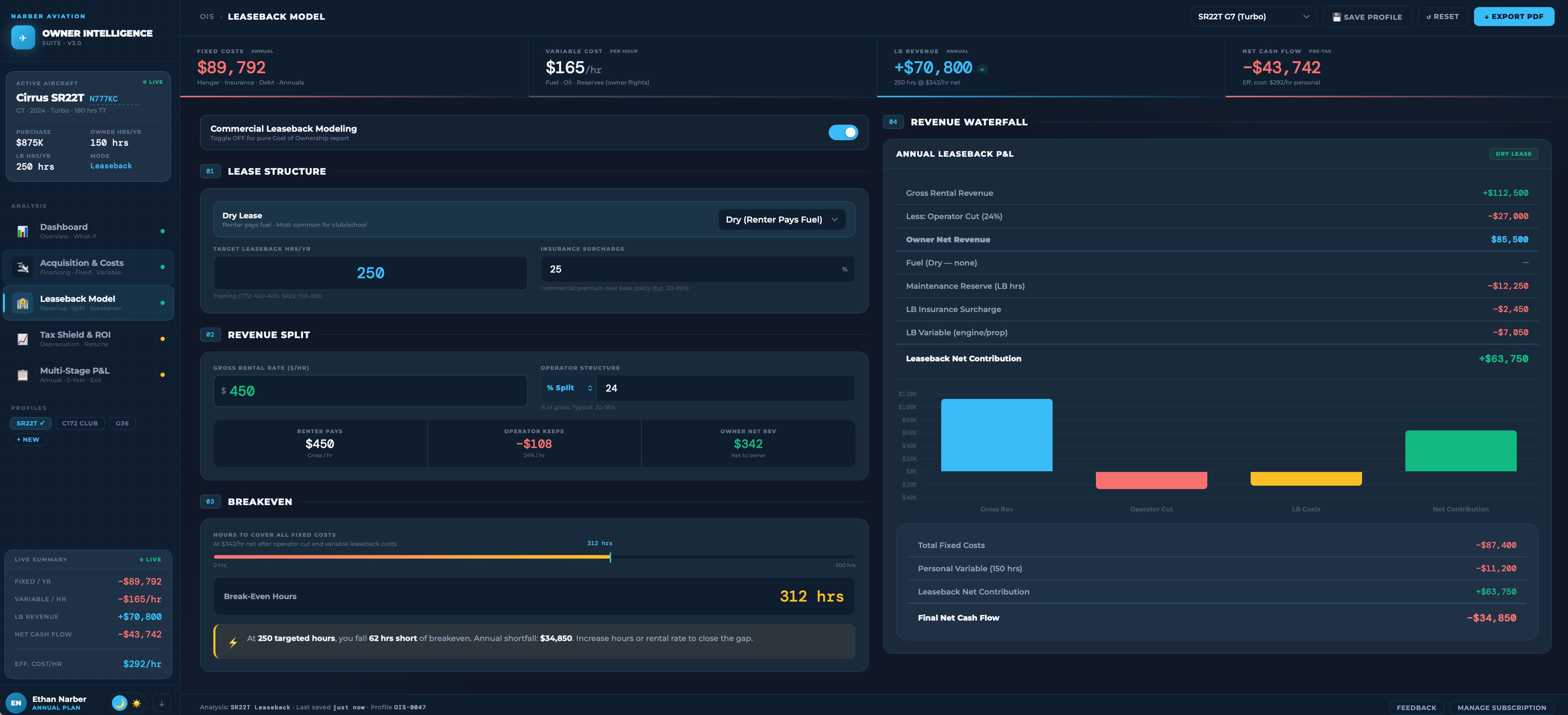

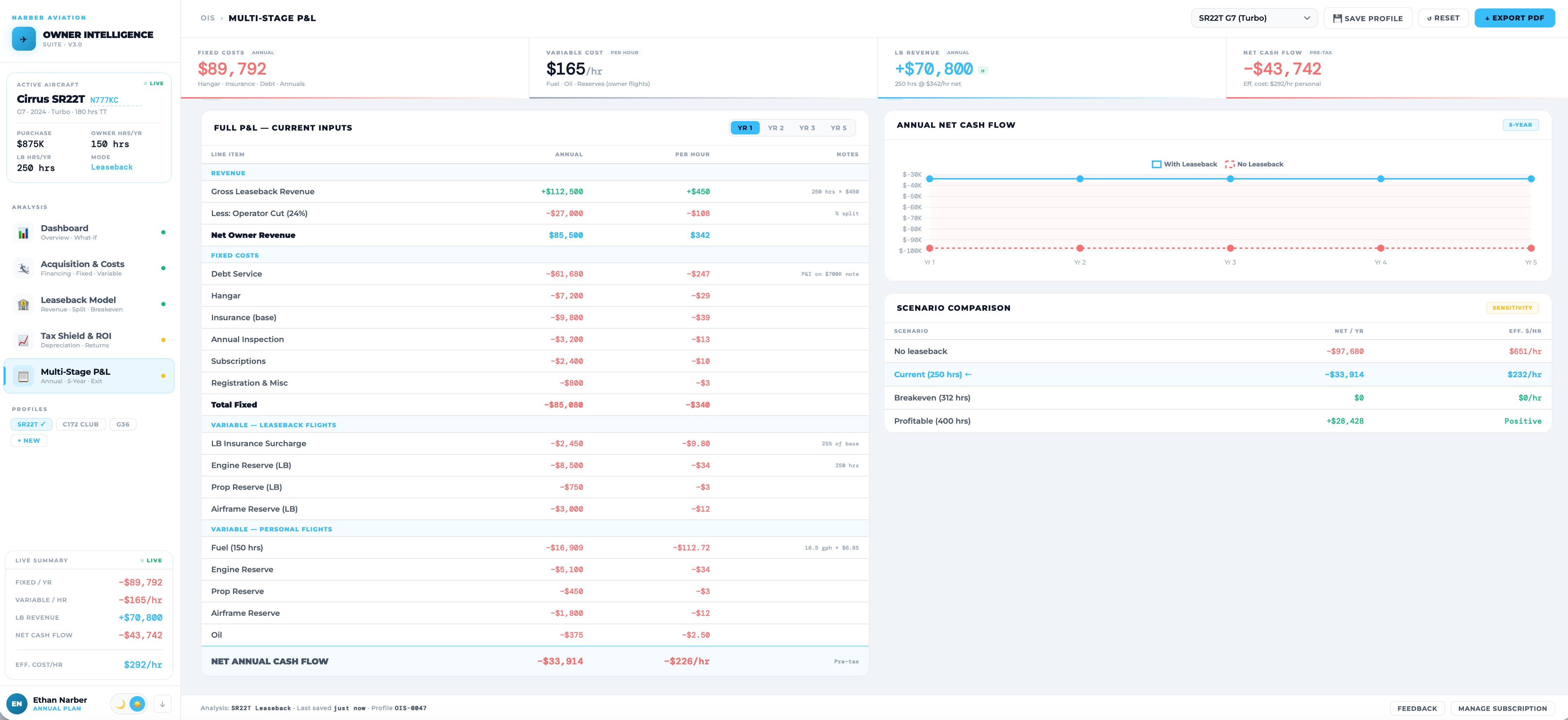

Model the true cost of ownership in minutes. Run leaseback economics with operator splits and breakeven analysis. Quantify your bonus depreciation tax shield. Project five-year equity at exit. One tool. Every aircraft.